Your Money

RENT OR BUY?

Make a winning financial decision when you move

Ann and Tracy Godfrey, both 78, have owned their two-story home in Golden Valley, Minnesota, for nearly 40 years. Their garden is a source of pride and joy, but tending it, they say, is getting to be too much. “We can’t do it anymore,” says Ann.

They want to move but also stay close to their friends, community and doctors, so they’ve limited their search to nearby homes. What they haven’t figured out is a question facing many older adults: “Should we buy our next place or rent it?”

“We’re leaning toward owning,” Tracy says, “but renting may turn out to be a better option.” Ann laughs: “Every time I think I’m ready to decide, there’s a big ‘but.’ ”

Selling the home you’ve lived in for decades can leave you with a pile of money at the closing, giving you the wherewithal to buy your next home with a hefty down payment or maybe even no mortgage at all. But that doesn’t necessarily make it the right choice.

Quality-of-life factors are important, and they’re where you should start, says Erin DiCarlo, founder of Massachusetts-based Dovetail Companies, which provides services to older adults facing major life transitions. “How do you see your future?” she asks. “What’s most important to you?”

But if the finances of buying versus renting play a role in your housing choice, here are some tips for working through the decision.

THINK ABOUT YOUR TIME FRAME

“If you’re in it for the short run, usually renting is better,” says Daryl Fairweather, chief economist at Redfin, the online real estate brokerage. In general, that means renting if you plan to stay less than five years.

Why? When you buy, you’re not just paying the home’s price and perhaps committing to a mortgage; you’re also typically on the hook for 2 to 5 percent of the purchase price in closing costs. And when you sell, you’ll likely lose 8 to 10 percent of the sales price to transaction costs. In general, buying wins if your time horizon is 10 years or more. “The longer you stay in the home, the more opportunity you have for that home to go up in value,” says Fairweather. “The longer you stay in the home, the better off you are financially.”

So you should ask yourself serious questions about changes in your health or your family situation that might require yet another move. The typical 65-year-old can expect to live about two more decades and has a 28 percent chance of spending 90 days or more in a nursing home, according to the Urban Institute; 15 percent of older adults will spend more than two years in one.

DIG INTO HOMEOWNER FINANCES

Separate from a mortgage, the average American homeowner spends almost $25,000 annually, or more than $2,000 monthly, on home expenses, according to Real Estate Witch, an industry publication. That number, up sharply in recent years, includes property taxes, insurance, repairs and maintenance.

Research can inform a budget plan. You can learn about property taxes from your real estate agent, as well as the main real estate platforms like Realtor.com, Zillow.com and Redfin.com. County assessor or auditor websites offer public portals to look up current assessed value and tax bill by address. To get an idea of home insurance costs, you might call two or three local independent agents. Your monthly mortgage payment will depend on the home’s cost, interest rates, length of the mortgage and the size of your down payment.

Over the long term, ownership also gives you the possibility of profiting from price appreciation. Home prices aren’t guaranteed to rise, however, and, as mentioned, transaction costs cut into potential profits.

CONSIDER RENTAL FINANCES

Calculating monthly costs is much easier for renters: Add up your monthly rent, utilities and renters insurance. Rents have risen 5.1 percent on an annualized basis over the past five years, according to the Bureau of Labor Statistics, though hikes have slowed since 2023. The cost of renters insurance, which covers personal property but not structures, has increased 2.9 percent annually.

As for the long-term financial consequences: Unlike a fixed-rate mortgage payment, your rent could rise year after year. But, assuming you have cash left over from the sale of your home, you’d keep more of it than you would if you had used it on a down payment for a purchase. You could set it aside for other purposes, perhaps putting it in the bank or investing it in the hopes of getting higher returns. Either way, you’d have less of your wealth tied up in real estate. “One of the main benefits of renting and having liquid, fungible cash is diversification,” says Kristian Fors, a research fellow at the Independent Institute in Oakland, California.

MIND THE GAP

Before making any final comparisons between renting and buying, research local conditions and estimate your down payment on any purchase. Right now, on average, renting is usually cheaper, according to Redfin. That estimate reflects that most rental stock consists of apartments, while most homes for sale are single-family houses. It’s also a function of mortgage rates, which have risen above 6 percent in recent years.

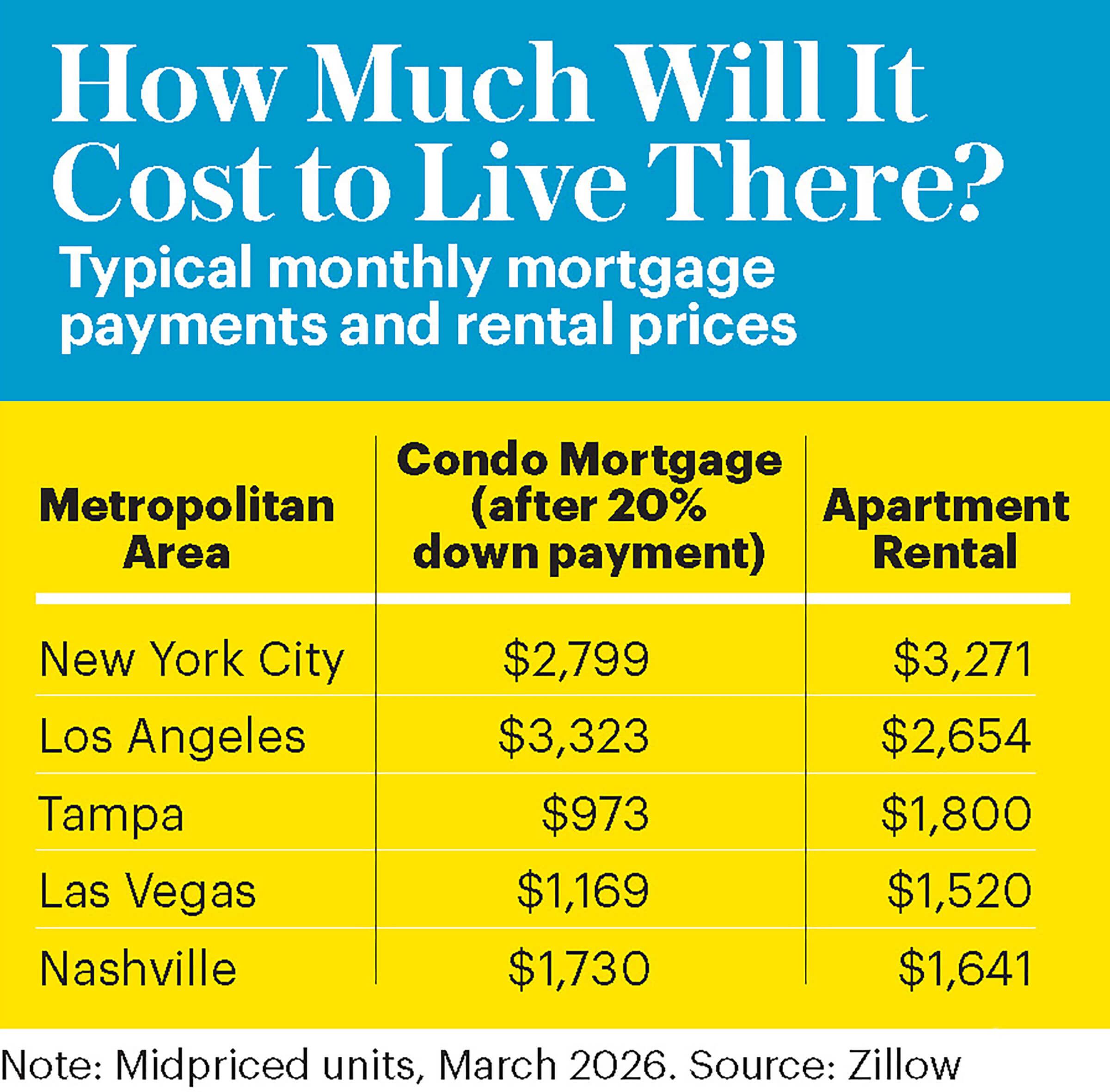

If the choice is an apartment rental versus a condominium purchase—more of an apples-to-apples comparison—the numbers are different. Among midpriced properties as of March, the typical monthly apartment rent is $1,757, while the typical condo mortgage payment is $1,698, reports Zillow. By Zillow’s calculations—which assume a 20 percent down payment on purchases and a 6.18 percent, 30-year fixed-rate mortgage but don’t include maintenance, taxes or insurance—rents exceed mortgage payments in 39 of the top 50 U.S. metropolitan areas.

If you’re rolling over the profits from a home sale into a new purchase, your mortgage bill could be even lower. For example, if you make a $150,000 down payment on Zillow’s typical condo, your monthly payment would drop nearly $500 to $1,206. “The less you borrow, the less you are going to be paying in interest and the less expensive it is going to be to buy that home,” Fairweather says. To dig deeper into the finances of your housing decision, you can check out AARP’s Rent vs. Buy Home Calculator; to find it, go to aarp.org/calculators and click on Personal Finance.

Chris Farrell is a journalist and the author of books including Purpose and a Paycheck: Finding Meaning, Money, and Happiness in the Second Half of Life.